The

2022 housing market has been defined by two key things: inflation and rapidly

rising mortgage rates. And in many ways, it’s put the market

into a reset position.

As

the Federal

Reserve (the Fed) made moves this year to try to lower inflation,

mortgage rates more than doubled – something that’s never happened before

in a calendar year. This had a cascading impact on buyer activity, the balance

between supply and demand, and ultimately home prices. And as

all those things changed, some buyers and sellers put their plans on hold and

decided to wait until the market felt a bit more predictable.

But what

does that mean for next year? What everyone really wants is more stability in

the market in 2023. For that to happen we’ll need to see the Fed bring

inflation down even more and keep it there. Here’s what housing market experts

say we can expect next year.

What’s Ahead

for Mortgage Rates in 2023?

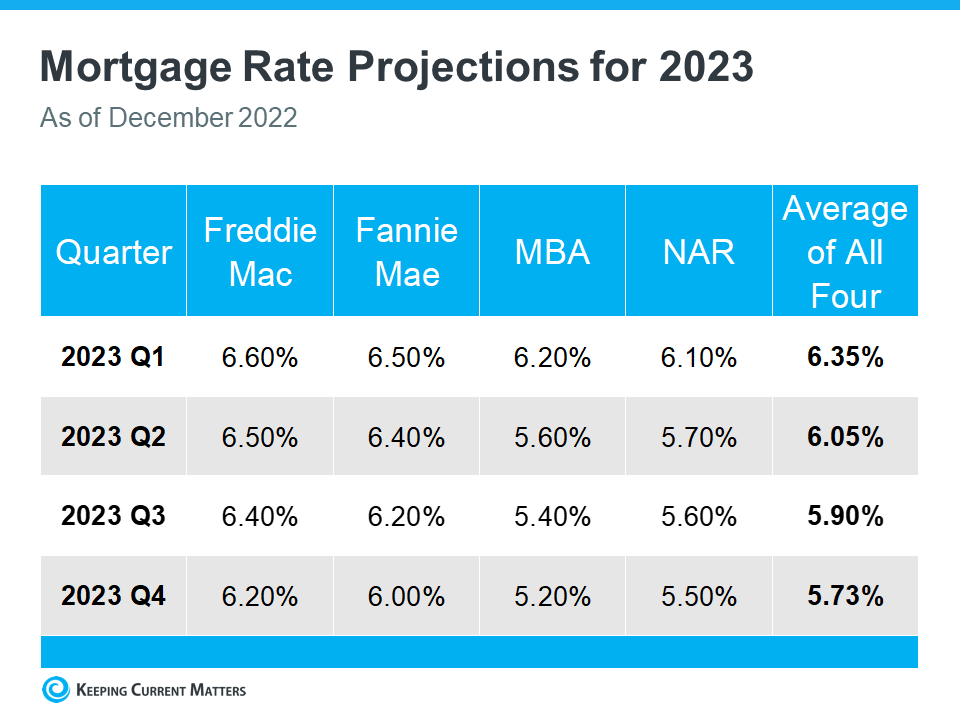

Moving

forward, experts agree it’s still going to be all about inflation. If inflation

is high, mortgage rates will be as well. But if inflation continues to fall, mortgage rates will likely respond. While there

may be early signs inflation is easing as we round out this year, we’re not out

of the woods just yet. Inflation is still something to watch in 2023.

Right

now, experts are factoring all of this into their mortgage rate forecasts for

next year. And if we average those forecasts together, experts say we can

expect rates to stabilize a bit more in 2023. Whether that’s between 5.5% and

6.5%, it’s hard for experts to say exactly where they’ll land. But based on the

average of their projections, a more predictable rate is likely ahead (see

chart below):

That

means, we’ll start the year out about where we are right now. But we could see

rates tick down if inflation continues to drop. As Greg McBride, Chief

Financial Analyst at Bankrate, explains:

“. . . mortgage rates could

pull back meaningfully next year if inflation pressures ease.”

In the

meantime, expect some volatility as rates will likely fluctuate in the weeks

ahead. If we see inflation come back under control, that would be good news for

the housing market.

What Will

Happen to Home Prices Next Year?

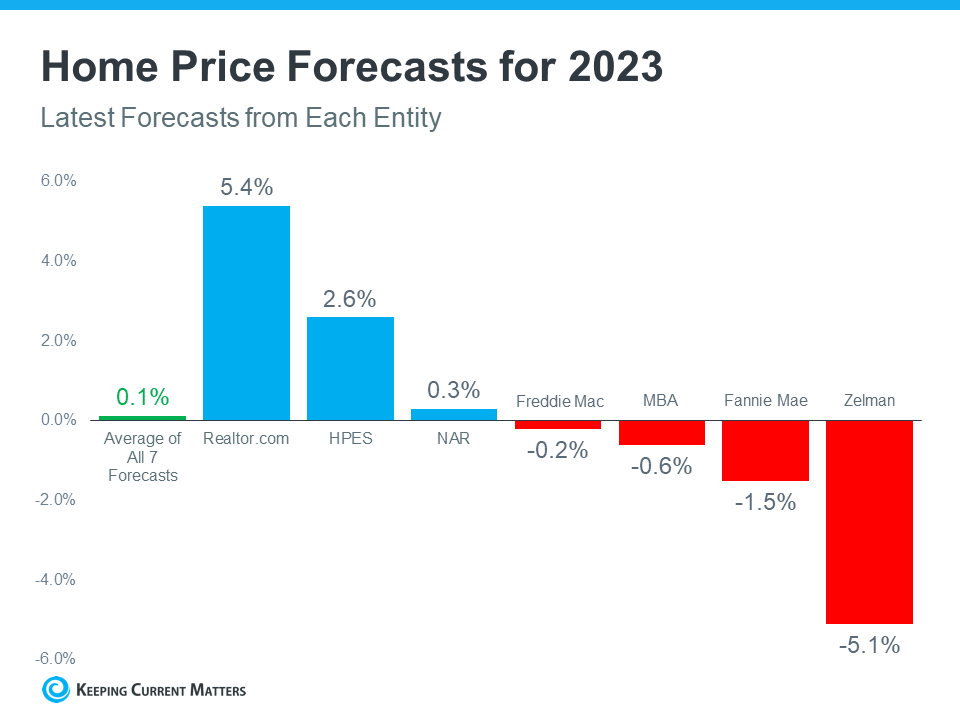

Homes

prices will always be defined by supply and demand. The more buyers and fewer

homes there are on the market, the more home prices will rise. And that’s

exactly what we saw during the pandemic.

But this

year, things changed. We’ve seen home prices moderate and housing supply grow

as buyer demand pulled back due to higher mortgage rates. The level of

moderation has varied by local area – with the biggest changes happening in

overheated markets. But do experts think that will continue?

The

graph below shows the latest home price forecasts for 2023. As the different

colored bars indicate, some experts are saying home prices will appreciate next

year, and others are saying home prices will come down. But again, if we take

the average of all the forecasts (shown in green), we can get a feel for what 2023 may hold.

The

truth is probably somewhere in the middle. That means nationally, we’ll likely

see relatively flat or neutral appreciation in 2023. As Lawrence Yun, Chief

Economist at the National Association of Realtors (NAR), says:

“After a big boom over the past two years, there will essentially

be no change nationally . . . Half of the country may experience small price gains, while the

other half may see slight price declines.”

Bottom Line

The 2023

housing market is going to be defined by mortgage rates, and rates will be

determined by what happens with inflation. The best way to keep a pulse on what

experts are projecting for next year is to lean on a trusted real estate

advisor.

Knock Buyer-Seller Market Index shows that 15 markets saw home prices fall by 10% or more from their highs set this spring, pushing more markets into buyer-market territory

Reno, Nevada, Winston-Salem, North Carolina, and Boise, Idaho, saw home prices drop the most from their peak prices

Providence, Rhode Island, and Salisbury, Maryland, were the only markets where home prices have remained at their peaks set this summer

Home prices in 42 markets are projected to fall further from their record highs by September 2023

Twenty-seven of the nation's 100 largest markets will favor buyers by September 2023, up from 16 markets now

NEW YORK, Oct. 31, 2022 /PRNewswire/ -- The cooling trend that is engulfing the U.S. housing market is expected to continue with more markets seeing home prices decline by this time next year as the shift to a buyer's market continues to take hold, according to the Knock Buyer-Seller Market Indexreleased today. The Index, which analyzes key housing market metrics to measure the degree to which the nation's 100 largest markets favor home buyers or sellers, found home prices in 98 markets in September were below their peak price this spring. Providence, Rhode Island, and Salisbury, Maryland, were the only markets where home prices have remained at their peaks set earlier this year.

In 15 markets, prices dropped by 10% and prices in 42 markets are projected to fall further from their 2022 records by September 2023. The total number of buyers' markets increased to 16, more than double from August. This is expected to grow to 27 by September 2023.

In a sign of the current market where high home prices and rising interest rates have pushed many buyers to the sidelines, just over 1.8 million homes had traded hands across the nation's largest 100 housing markets through the first nine months of 2022 -- less than during the same time frame in each of the past four years. Although still low, the supply of homes for sale has grown steadily throughout 2022 as median days on market increased to 20 in September – up by one full week from a year ago.

The average sale-to-list ratio, which measures how close homes are selling to their asking prices, fell to 99% in September, the lowest level since February 2021 and down from 100.3% in May when home prices peaked across the nation.

"Based on our findings, the shift to a more balanced market is still in its early stages. We expect that this much-needed reset will persist through much of 2023, and although prices will again begin to rebound they likely won't return to their peaks for the foreseeable future," said Knock Co-Founder and CEO Sean Black. "While many drivers of the housing market like demographics and record low unemployment have not changed, the combination of higher rates and home prices have put affordability at the worst levels in 30 years with entry-level monthly payments set to be 34% higher in 2022 vs 2021. The good news is that as prices soften and rates stabilize once the Fed is done with its aggressive rate hike campaign, hopefully after its meeting in November, buyers will be ready to re-enter the market and sellers will retain the majority of the equity gains they've seen in the last two years."

West and South dominate the 15 markets with the largest price declines

Nationally, the median home price was up 6.6% to $388,000 year-over-year in September, but down 5.4% from its peak of $410,000 in May. Although seasonality plays a factor in home prices, the rate at which prices are appreciating is well below the double-digit growth seen over the past two years.

Fifteen markets saw prices drop by 10% or more in September from their price peaks, which were set between April and June. Seven of those markets are in the West, another seven are in the South and just one, Bridgeport, Connecticut, is in the Northeast. Reno, Nevada, Winston-Salem, N.C., and Boise City, Idaho saw the biggest declines from their peak prices, falling 14%, 13.1% and 13.1%, respectively.

According to the Index, home prices in 13 of the 15 markets will grow year-over-year, but are expected to remain below their 2022 peak pricing through September 2023. Winston-Salem, North Carolina (10.3%), Fayetteville, Arkansas (9.1%), and Seattle, Washington (8.9%) will see the largest year-over-year price gains. Home prices in Boise, Idaho, and Las Vegas, Nevada, are projected to decline further by this time next year.

Markets Seeing the Biggest Declines From Peak Pricing

Market

Peak price

Month of peak price

Current median sale price

% change

Forecasted median sale price

YoY price change (2022-23)

National

$410,000

May

$388,000

-5.4 %

$414,000

6.6 %

Reno, Nev.

$570,000

May

$490,000

-14.0 %

$491,000

0.2 %

Winston-Salem, N.C.

$282,000

June

$245,000

-13.1 %

$270,000

10.3 %

Boise City, Idaho

$535,000

May

$465,000

-13.1 %

$448,000

-3.6 %

Austin-Round Rock- Georgetown, Texas

$590,000

May

$515,000

-12.7 %

$535,000

3.8 %

New Orleans-Metairie, La.

$315,000

June

$275,000

-12.7 %

$286,000

3.9 %

San Jose-Sunnyvale- Santa Clara, Calif.

$1,600,000

April

$1,400,000

-12.5 %

$1,443,000

3.1 %

San Francisco-Oakland- Berkeley, Calif.

$1,300,000

April

$1,145,000

-11.9 %

$1,148,000

0.3 %

Fayetteville-Springdale-Rogers, Ark.

$345,000

June

$306,000

-11.3 %

$334,000

9.1 %

Savannah, Ga.

$333,600

June

$296,000

-11.3 %

$308,000

3.9 %

Pensacola-Ferry Pass- Brent, Fla.

$338,000

June

$300,000

-11.2 %

$319,000

6.2 %

Las Vegas-Henderson- Paradise, Nev.

$450,000

May

$400,000

-11.1 %

$386,000

-3.5 %

Ogden-Clearfield, Utah

$499,900

June

$445,000

-11.0 %

$458,000

3.0 %

Naples-Marco Island, Fla.

$625,000

May

$560,000

-10.4 %

$584,000

4.3 %

Bridgeport-Stamford- Norwalk, Conn.

$639,000

June

$574,000

-10.2 %

$595,000

3.6 %

Seattle-Tacoma- Bellevue, Wash.

$750,000

April

$675,000

-10.0 %

$735,000

8.9 %

By next year, 42 markets will see price declines from their peak

Home prices in 42 major housing markets are projected to fall further from their 2022 record highs by next September. Fifteen of the 42 markets are in the South, including three of the 10 markets with the largest forecasted price drops. Fifteen are in the West -- home to some of the most expensive markets in the nation. The remaining seven and five markets forecasting prices below this summer's peak are in the Midwest and Northeast, respectively. Bridgeport, Connecticut, is forecasted to see the largest price drop (-7.8%), while Springfield, Missouri, will lead the Midwest with a projected price decline of 3.9%.

The top 10 markets with forecasted price drops through September 2023 are: Boise, Idaho (-16.2%); Lakeland, Florida (-14.2%); Las Vegas, Nevada (-14.2%); Reno, Nevada (-13.9%); San Francisco, California (-11.7%); San Jose, California (-9.8%); Austin, Texas (-9.3%); Oxnard, California (-9.3%); New Orleans, Louisiana (-9.3%) and Ogden, Utah (-8.3%).

In 15 of the 25 markets with the largest projected median sale price declines, prices peaked at well above the national high of $410,000. The median sale price peaked at $1.3 million and $1.6 million in San Francisco and San Jose, California, in April 2022, respectively.

Buyers' markets will grow from 16 to 27 by next year; sellers' markets will shrink to 43

Despite the cool-off – a majority – 51 markets – remained sellers' markets in September, down from 83 in August. Housing markets that still favor sellers are generally smaller. Only two of the top 10 seller's markets in September (Rochester, New York and Hartford, Connecticut) have populations of more than 1 million people.

Sixteen markets significantly favored buyers in September. Austin, Texas; Boise, Idaho; Colorado Springs, Colorado; Detroit, Michigan; Jacksonville, Florida; Las Vegas, Nevada; Los Angeles, California; Nashville, Tennessee; Reno, Nevada; Ogden, Utah; Phoenix, Arizona; Riverside, California; Salt Lake City, Utah; San Diego, California; San Francisco, California; and San Jose, California, were in buyer territory last month. Thirty-three markets were neutral, offering no advantage to either sellers or buyers.

Top Buyers' Markets in September 2022

Rank

Market

Median sale price

Inventory

Inventory YoY change

Homes sold

Median days on market

National

$388,000

441,714

4.2 %

107,930

20

1

Phoenix-Mesa-Chandler, Ariz.

$449,000

19,327

67.7 %

2,463

29

2

Ogden-Clearfield, Utah

$445,000

1,710

83.5 %

343

29

3

San Francisco-Oakland- Berkeley, Calif.

$1,145,000

5,174

10.4 %

1,165

23

4

Las Vegas-Henderson- Paradise, Nev.

$400,000

10,992

71.3 %

1,197

26

5

Salt Lake City, Utah

$505,000

2,344

46.3 %

508

21

6

San Diego-Chula Vista- Carlsbad, Calif.

$800,000

4,186

20.5 %

1,166

21

7

Los Angeles-Long Beach-Anaheim, Calif.

$875,000

16,438

1.1 %

2,981

35

8

Reno, Nev.

$490,000

2,081

55.9 %

300

26

9

Riverside-San Bernardino-Ontario, Calif.

$530,000

12,304

16.9 %

1,961

32

10

Nashville-Davidson- Murfreesboro-Franklin, Tenn.

$445,000

6,707

29.4 %

1,147

26

11

Jacksonville, Fla.

$347,000

5,230

22.7 %

811

29

12

San Jose-Sunnyvale- Santa Clara, Calif.

$1,400,000

1,659

7.7 %

587

19

13

Detroit-Warren-

Dearborn, Mich.

$250,000

8,553

8.8 %

1,973

18

14

Colorado Springs, Colo.

$435,000

2,631

66.1 %

584

18

15

Austin-Round Rock- Georgetown, Texas

$515,000

8,499

71.2 %

951

36

16

Boise City, Idaho

$465,000

2,617

50.1 %

397

N/A

By September 2023, the U.S. housing market will skew more toward buyers. Twenty-seven of the 100 major housing markets are projected to favor buyers, 30 will be neutral and 43 will favor sellers.

According to the Index, slightly over a million homes are projected to be sold between January and September 2023, down from 1.8 million during the same period in 2022. The median sale price across the nation is projected to remain flat through the beginning of next year. Prices will start to rise in May and are forecast to exceed $412,000 by May 2023, surpassing this year's record of $410,000. Inventory throughout the U.S. is expected to decline 5.7% and median days on market will increase to 36 days by September 2023.

For home buyers and prospective property investors, this could mean encountering the most favorable national market seen in recent years. For sellers, the most favorable months next year are likely to be March and April, when the market is projected to linger in neutral territory, before it starts to significantly favor buyers by June 2023.

The index comprises six measures: the ratio of average sale to asking price, number of homes sold, number of active listings, median days on market, median sale price and the rolling supply of homes in a given month. It uses data on more than 150 million properties in the nation's 100 largest, most active metropolitan areas since 2017 from a number of sources. Median days on market data is not available for seven of the 100 largest markets (Boise, Idaho; Richmond, Va.; Seattle; Allentown, Penn.; Portland, Maine; New Haven, Conn. and Bridgeport, Conn.)

Index values range from -4 to 4, with lower values indicating a relatively favorable market for buyers and higher values indicating a relatively favorable market for sellers. Index values ranging around zero denote a somewhat neutral housing market.

With over 20 years experience in Fairfield County real estate, Rob has seen both the market’s high and low points. His approach to his clients has remained the same. Survey the market daily to understand where it is trending, work with a limited number of seller and buyer clients to give them the best possible service, and establish a rapport of openness and honesty.

On average, Rob’s listings sell at nearly 95% of asking price, testament to his outstanding pricing acumen and understanding of market conditions. He has served as the Chairman of the Technology Committee for the Mid-Fairfield County Association of Realtors and as its representative on the state level. Rob resides in Westport with his family.

{kind=link}

{kind=link}